What Is a High Yield Savings Account? 5 Powerful Ways to Maximize Income

If you keep your hard-earned money sitting in a traditional brick-and-mortar bank, you are actively losing purchasing power to inflation every day. The solution to this common financial trap is simple: moving your cash into a specialized banking vehicle designed to optimize growth. But what is a high yield savings account, and how exactly does it work to protect your wealth?

A high-yield savings account (HYSA) is a federally insured deposit account that pays an interest rate significantly higher than the national average for a standard savings account. While a legacy bank might offer a nearly invisible return on your money, top-tier financial institutions use modern online infrastructure to pass massive interest savings directly back to you.

This comprehensive guide breaks down everything you need to know about navigating the banking market, choosing the best vehicle for your cash, and building a secure emergency fund.

1. Understanding the Basics: What Is a High Yield Savings Account?

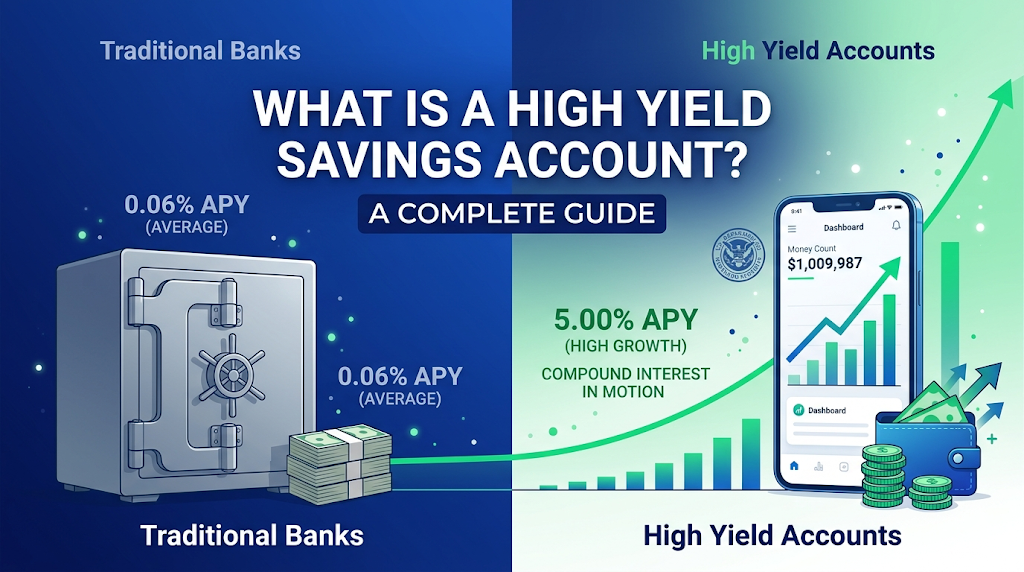

To understand what is a high yield savings account, it helps to look at the structural shift in modern banking. Traditional banks maintain thousands of physical branches, paying massive overhead costs for real estate, tellers, and local utilities.

Online-first financial institutions don’t have those massive overhead expenses. Because they operate digitally, they can afford to pay customers significantly more to house their cash deposits.

Historically, according to data monitored by the Federal Deposit Insurance Corporation (FDIC), traditional bank accounts pay an average interest rate of roughly 0.06% Annual Percentage Yield (APY). In stark contrast, a quality high-yield savings option frequently offers rates 10 to 12 times higher, completely transforming how your liquid net worth scales over time.

2. The Financial Magic of Compound Interest

The primary motor running behind a high-yield vehicle is compound interest. Compound interest is simply earning interest on top of the interest you have already accumulated.

When you leave cash in a high-yield environment, your balance grows slightly at the end of every monthly cycle. The following month, the bank calculates your interest payment based on that new, larger balance. Over several years, this creates an exponential growth curve that turns passive saving into an automated wealth-building routine.

For example, if you add money regularly, your balance accelerates because you are earning returns on a continuously expanding financial base.

3. Traditional Savings Accounts vs. High Yield Savings Accounts

Seeing the raw mathematical difference makes it clear why your choice of financial vehicle matters. Let’s compare exactly what happens over a 5-year timeline if you deposit a baseline emergency fund of $10,000 into a traditional legacy account versus a top-performing digital alternative.

| Feature / Metric | Traditional Savings Account | High Yield Savings Account |

| Average APY | ~0.06% | ~4.50% to 5.00% |

| Initial Deposit | $10,000 | $10,000 |

| Year 1 Balance | $10,006 | $10,450 |

| Year 5 Balance | $10,030 | $12,461 |

| Total Interest Earned | $30 | $2,461 |

| Physical Branches | Yes, thousands | Rarely (Mostly Digital) |

By ignoring the question of what is a high yield savings account and keeping money in a traditional space, a saver leaves over $2,400 on the table in this scenario. Both types of accounts feature identical federal safety nets, meaning the legacy choice carries a massive opportunity cost with zero added security.

4. 5 Crucial Benefits of Utilizing an HYSA

Investing in volatile stock options isn’t always the right move for cash you need to access quickly. An HYSA bridges the gap between total security and wealth optimization.

1. Absolute Federal Security

Just like your local neighborhood branch, reputable online banks carrying these high-interest vehicles are backed by the federal government. Your funds are protected up to $250,000 per depositor, per insured institution, through the FDIC or the NCUA (for credit unions).

2. Immediate Cash Liquidity

Unlike a Certificate of Deposit (CD) which locks your money away for set terms ranging from six months to five years, high-yield savers keep your funds highly accessible. You can initiate a transfer back to your primary checking ecosystem whenever an unforeseen expense pops up.

3. Protection Against Inflation

While cash stashed under a mattress or inside a zero-interest checking account actively devalues due to macro-economic inflation, an HYSA acts as a financial shield, helping your cash maintain its baseline purchasing power over time.

4. Minimum Barriers to Entry

Many top-tier modern digital banking institutions have completely removed old-school barriers. You can easily find accounts featuring zero mandatory monthly maintenance fees and no strict minimum balance constraints to get started.

5. Automated Financial Habits

Most digital financial platforms provide robust mobile tools that allow you to set up recurring automated transfers. Directing a fixed percentage of your paycheck directly into your high-yield bucket keeps your savings goals perfectly on track without manual effort.

5. What to Look For When Picking an Account

Not all banking institutions are built equally. When you begin comparing different financial providers, keep these critical benchmarks in mind:

- Fee Schedules: Read the fine print to confirm there are zero monthly maintenance fees, statement fees, or hidden ACH transfer penalties.

- Compounding Schedules: Look for financial institutions that calculate and apply interest daily rather than monthly or quarterly. Daily compounding accelerates your long-term return curve.

- Transfer Efficiency: Ensure the institution supports fast electronic transfers or links cleanly to your peer-to-peer payment apps for smooth access.

- User Interface Quality: Since you will manage this account almost entirely online, a highly-rated, stable mobile app makes tracking your goals much simpler.

6. Frequently Asked Questions

Can the interest rate on a high yield savings account change?

Yes. High-yield savings options operate on variable rates. Banks adjust their yield percentages up or down based on macroeconomic policy changes executed by the Federal Reserve System. When the Fed raises rates, your account yield typically scales up alongside it.

Is my money completely safe in an online bank?

Yes, provided the bank is explicitly verified as an FDIC member. Federal insurance treats registered online banks exactly the same as physical brick-and-mortar operations.

How long does it take to move money out of an HYSA?

Electronic ACH transfers between separate financial institutions generally take between 1 to 3 business days to clear completely. Many modern online ecosystems now offer specialized debit cards or linked checking options for immediate emergency access.

Are the interest earnings subject to taxes?

Yes. The interest income you accumulate in any standard savings vehicle is treated as taxable income by the IRS. Your financial provider will issue a Form 1099-INT at the start of every tax season detailing your total yearly earnings.

Summary Takeaway: An HYSA offers a risk-free, federally backed ecosystem to ensure your cash preserves its value. By shifting away from low-yield traditional legacy systems, you ensure your money works just as hard as you do.

You might also want to check these posts to learn more about what is a high yield savings account: